The ultimate guide to understanding your credit score

What is a credit score?

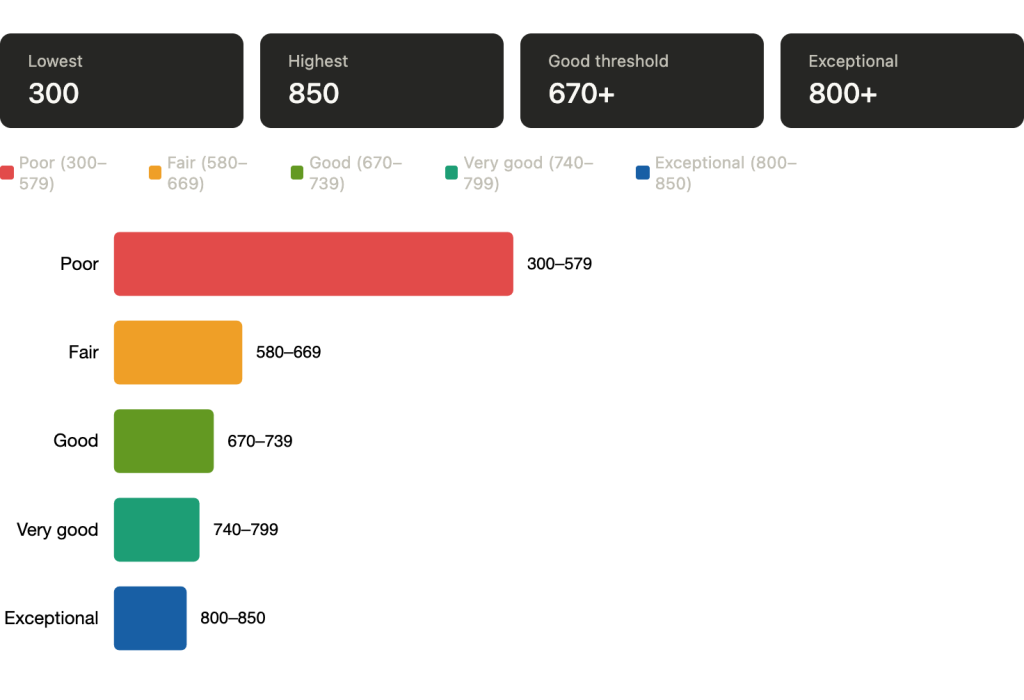

A credit score is a three-digit number that represents how responsibly you’ve managed credit over time. Lenders, landlords, and financial institutions use it to assess risk when you apply for credit cards, loans, housing, or other financial products. Most credit scores fall on a scale of 300 to 850. The higher your score, the lower the perceived risk you pose to a lender. Your credit score is generated from the information in your credit report — a detailed record of your borrowing history maintained by the three major credit reporting agencies: Equifax, Experian, and TransUnion.

This article is for educational purposes only and does not provide financial advice.

Why does your credit score matter?

Your credit score can affect more than just loan approvals. It may influence:

- Loan and credit approvals – lenders use your score as a primary risk indicator

- Interest rates – a higher score often means access to lower rates, which reduces the total cost of borrowing

- Security deposits – landlords and utility providers sometimes require larger deposits from applicants with lower scores

- Insurance premiums – some insurers factor in credit-based scores when determining rates

- Employment screening – certain employers, particularly in financial industries, may review credit as part of a background check.

Understanding your scores give you a clear picture of what lenders see when you apply for credit.

How is a credit score calculated?

Credit scoring models like FICO and VantageScore analyze five main categories from your credit report. Here’s how each one typically factors into your score:

- Payment History (35% of your score): payment history is the single most influencial factor. It tracks whether you’ve paid your bills on time across credit cards, loans and other accounts.

What can negatively affect this factor:

- Late or missed payments

- Accounts sent to collections

- Bankruptcies or foreclosures

Even one missed payment can have a noticeable impact, particularly if your credit history is limited.

2. Credit Utilization (30% of your score): Credit utilization is the percentage of your available revolving credit that you’re currently using.

Example:

- Credit limit: $2,000

- Current balance: $600

- Utilization rate: 30%

Most financial experts suggest keeping utilization below 30%. Lower is generally better. High utilization signals to lenders that you may be over-relying on credit.

3. Length of Credit History (~15% of Your Score):

This factor considers:

- How long your oldest account has been open

- How long your newest account has been open

- The average age of all your accounts

A longer credit history typically works in your favor because it gives lenders more data to evaluate. This is one reason financial advisors often recommend keeping older accounts open, even if you no longer use them regularly.

4. Credit Mix (~10% of Your Score):

Lenders like to see that you can responsibly manage different type of credit. Your credit mix may include:

- Revolving credit – credit cards, line of credit

- Installment loans – mortgages, auto loans, student loans, personal loans

Having a healthy mix can work in your favor, though this factor carries less weight than payment history or utilization. You shouldn’t open unnecessary accounts just to diversify your mix.

5. New Credit Activity (~10% of Your Score):

Each time you apply for new credit, a hard inquiry is recorded on your report. Multiple hard inquiries in a short window can temporarily lower your score.

Note: Rate shopping for a mortgage or auto loan within a short period (typically 14–45 days) is often treated as a single inquiry by scoring models so it’s less penalizing than applying for multiple credit cards.

FICO vs. VantageScore: What’s the difference?

Two models dominate credit scoring in the U.S.:

FICO® is the most widely used by lenders and banks. It’s been the industry standard for decades and weighs the five factors above.

VantageScore was developed jointly by the three major bureaus. It uses a similar framework but may weight factors slightly differently and can score consumers with shorter credit histories.

Both use the 300–850 range. You may see different scores from each, which is normal.

When should you check your credit score?

Regularly reviewing your credit helps you stay informed and catch potential issues early. Consider checking your score or report when:

- You’re planning a major purchase like a home or car

- You’ve been unexpectedly denied for credit

- you’re exploring debt relief or consolidation options

- You want to establish a financial baseline before making big decisions

- You suspect identity theft or fraudulent activity

Under federal law, you’re entitled to one free credit report per year from each of the three major bureaus through AnnualCreditReport.com.

Can you improve your credit score?

Yes and often more quickly than people expect. The most impactful steps tend to be:

- Paying on time, every time – set up autopay for at least the minimum payment to avoid missed payments

- Reducing credit card balances – owering utilization can have a relatively fast effect

- Avoiding unnecessary new credit applications – each hard inquiry temporarily dips your score

- Keeping older accounts open – even inactive accounts contribute to your average account age

- Disputing errors on your credit report – naccurate information can unfairly drag down your score

Credit improvement isn’t instant, but consistent habits produce real results over time.

The bottom line

A credit score is a snapshot of your credit health based on your borrowing history. It’s calculated from five key factors: payment history, credit utilization, length of credit history, credit mix, and new credit activity.

A lower score doesn’t define you or limit your options permanently and understanding how scoring works is the first step toward improving it.

Want to dig deeper? Explore our guide on what affects your credit score or visit our Debt Help Options page to learn about approaches for managing your financial situation.